Release Date: 2025/01/22 07:00

Report by Huang Guan-Hao, Wealth Magazine

▲ The delay in the domestic electric bus policy requires the government to address industry development issues. (Photo by Peng Shijie)

In 2008, Taiwan produced its first domestically manufactured bus. However, after 17 years, electric buses now only make up 18% of the fleet. With just 6 years left until the goal of full electrification of buses by 2030, what challenges still need to be overcome?

In line with the global trend toward net-zero emissions, the Ministry of Transportation plans to replace all 11,700 diesel buses across Taiwan with electric buses by 2030, with a focus on domestic manufacturing. The policy outlines three stages: pilot, promotion, and popularization, each with different domestic production ratios and subsidy schemes. The goal is to support Taiwan's electric bus industry and create an estimated value of NT$170 billion by 2030.

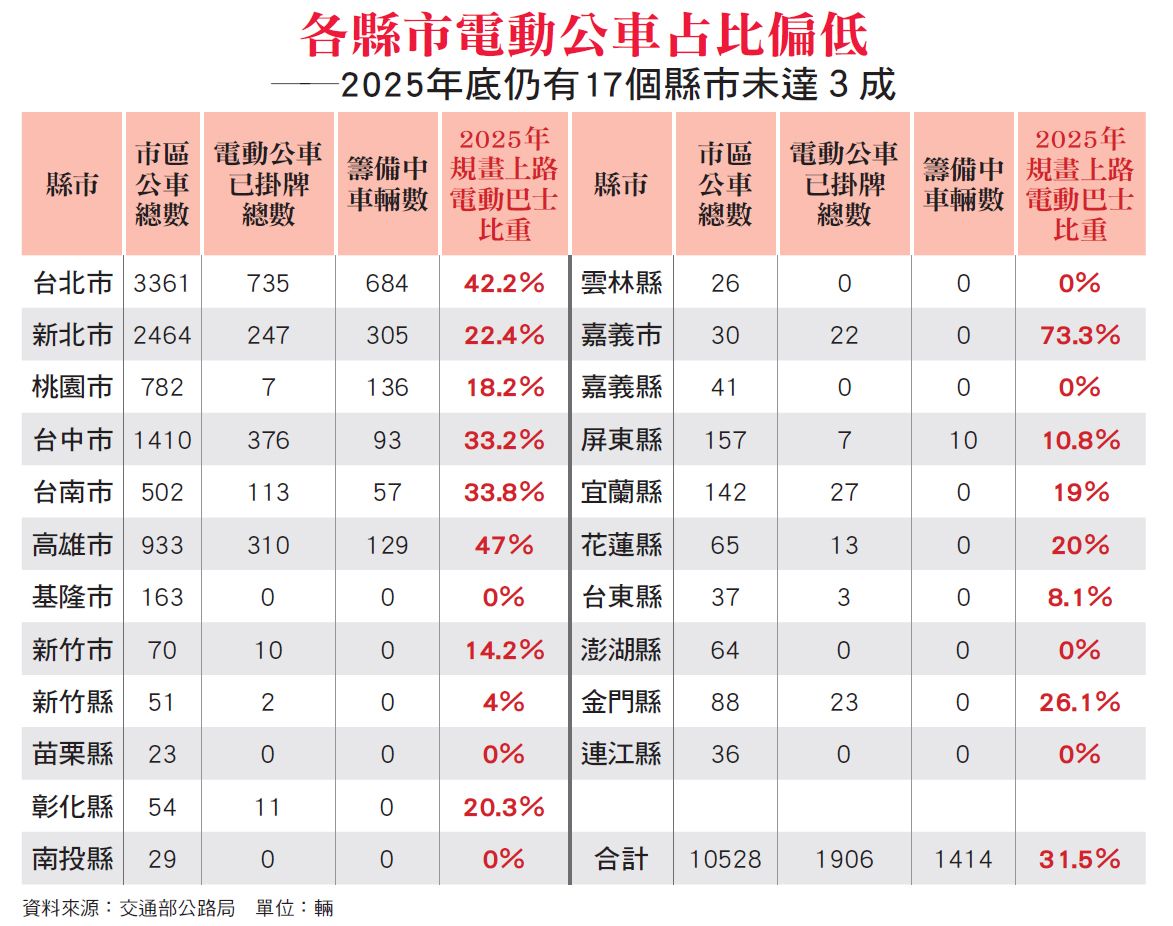

However, according to data from the Directorate General of Highways, the Ministry of Transportation approved subsidies for 2,080 buses in 2024, but only 1,404 were approved by local governments, with a completion rate of about 70%. Even more concerning, as of January 3, 2025, only 744 buses had been officially contracted. By the end of 2024, there were only 1,906 electric buses on the road in Taiwan, far from the government's target of 3,300 buses for that year.

Delayed Policy Implementation and Domestic Manufacturing Falling Short

Why has this situation occurred? An in-depth investigation reveals challenges at various levels, including the Ministry of Transportation, bus operators, and bus manufacturers.

Initially, after entering the policy promotion stage in 2023, bus operators were expected to start large-scale procurement. However, Zhao Jinwei, a specialist at the Ministry’s Department of Public Transportation and Supervision, admitted that the subsidy guidelines for the promotion phase were only issued in June 2024, delaying bus operators’ procurement plans. "However, the Ministry of Transportation will hold monthly meetings with local transportation agencies to review the progress. If procurement is seriously delayed, the subsidy amount will be reduced," Zhao stated.

Additionally, the government introduced the pilot phase policy to guide qualified domestic manufacturers, but after the pilot phase, only two manufacturers—Huade and Chengyun—had two models certified, limiting the supply available to bus operators and making it difficult to meet the varied needs of bus routes across counties and cities.

It wasn't until early June 2024 that Chuangyi Energy passed the review, and by late October, Honghua Advanced passed as well, bringing the total number of domestic manufacturers meeting local standards to four. Another manufacturer is expected to pass certification this year, expanding the range of available vehicle models for bus operators.

Besides delayed policies, manufacturers also face challenges in meeting delivery schedules. Each electric bus costs around NT$11 million, and manufacturers need NT$7.5 million in materials for each bus. If they want to prepare for 100 buses in advance, they need NT$750 million in capital, a massive financial burden that makes manufacturers hesitant to prepare materials before they secure contracts, further delaying delivery.

Industry players point out that certain components of electric buses, such as the front and rear axles and braking systems, come from Europe, and suppliers require 3-6 months to deliver these parts. Afterward, it takes about two months to manufacture the buses, and the entire process—including inspections, test drives, and regulatory approvals—takes over eight months. This results in limited production capacity and delays in deliveries.

Concerns About Material Preparation and Delivery Delays

Wu Ding-Fa, Chairman of Chengyun Motor, and Cai Yu-Qing, Chairman of Huade Energy, both agree that the government should help relax financing conditions for manufacturers' material preparations. With clear policies in the coming years, manufacturers would be able to prepare materials in advance, ensuring smooth delivery schedules.

Bus operators at the frontline feel the impact more acutely. Lü Qi-Long, Chairman of Zhongxing Bus Group, which operates around 1,500 buses in the Taipei area, stated that the high price and operational costs of electric buses are the biggest challenges for operators.

Historically, bus operators' main sources of income are threefold: first, farebox revenue; second, government subsidies for fare and loss-making routes; and third, advertising revenue, which is the only external source of income and the most profitable.

However, bus fares have remained stagnant for years, and operators rely heavily on government fare subsidies. For example, starting in 2025, the fare in Taipei will be NT$25, with the fare difference covered by the city government, especially for routes serving remote or sparsely populated areas, which are almost entirely subsidized. As a result, many bus operators have gone out of business in recent years, such as Sifang Electric Bus in Taichung and Hsinchu Bus, which had been in operation for over 100 years before ceasing operations last year.

The purchase price of a traditional diesel bus is around NT$3 million, while an electric bus costs about NT$11 million. Although the government offers subsidies of up to NT$6.8 million for the purchase, the cost difference remains significant, leading to low enthusiasm among operators to replace their fleets and a tendency to delay replacements.

At its core, the problem is financial. Although the government provides financial assistance, it only covers the cost of purchasing the buses and does not address the industry's pain points. For instance, the cost of one charging station is NT$1.2 million, and each station requires 40-50 charging piles, along with transformers. Setting up one station can cost over NT$60 million.

Moreover, most bus operators lack the space to build charging parking spaces. Even if they have the space, issues like insufficient power supply or inadequate capacity from Taiwan Power Company can arise. Operators estimate that the parking space for a diesel bus requires about 20 ping, but for an electric bus, the space needed for charging piles, power supply, transformers, and energy storage systems increases by over 50%. A parking lot with the same area can accommodate only 2/3 of the number of electric buses compared to diesel buses.

High Costs: Bus Purchases and Charging Stations Are Key Issues

Capital Bus Group, the leading bus operator in Taiwan with over 4,100 buses, is one of the most active companies in replacing its fleet with electric buses. By 2024, they are expected to replace about 1,000 buses with electric models. However, this process has not been without challenges. "We’ve invested so much, but when the landlord raises the rent after we’ve signed the contract and built the charging stations, we have no choice but to accept it," said Li Jianwen, General Manager of Capital Bus Group. He pointed out that land issues are a fundamental problem in Taiwan, and unless they are addressed, the policy could come to a halt by 2027.

As early as 2008, Huade Energy produced Taiwan's first electric bus, but after 18 years, the domestic electric bus industry has yet to reach significant scale. By the end of 2024, seven counties and cities had no electric buses, and 17 had less than 30% of their buses as electric, indicating that the adoption of electric buses is challenging and not just a problem for a few counties. This issue requires a comprehensive review by the central government.

Cai Yu-Qing also suggested that Taiwan’s electric bus industry should not be content with just the domestic market. It should use third-party evaluations to assess "competitiveness" to determine the reward mechanisms, or else the industry will only lead to price competition where operators prioritize subsidies over quality, undermining international competitiveness and ultimately resulting in a failed industry policy.